3700 Old Redwood Hwy Ste 200, Santa Rosa, CA, United States of America, 95403

Feeds

New Round of Funding from the USDA Coronavirus Food Assistance Program

For more information on the original round of funding from the US Department of Agriculture’s (USDA) Coronavirus Food Assistance Program (CFAP), please see our previous article.

On September 18, 2020, the USDA announced a new program and additional round of funding for agricultural producers who continue to face market disruptions, and associated costs, due to COVID-19.

Signup for CFAP 2 began September 21, 2020, and runs through December 11, 2020.

Brief Overview

Brief Overview

Eligibility and payment limits are separate from the CFAP 1 program. If you’ve already applied for CFAP 1, make sure to check eligibility for CFAP 2, evaluate your eligibility and if you want to apply, then apply as soon as possible. Applications can be submitted online via the USDA website or with your local Farm Service Agency office.

CFAP 2 was adapted to include more commodities that weren’t eligible in CFAP 1 including over 230 specialty crops.

CFAP 2 payments will be made for three new categories of payment calculations. The USDA has published a CFAP 2 payment calculator for producers to use when estimating payment amounts under each separate category.

Access a full list of eligible commodities and the payment calculator on the USDA website.

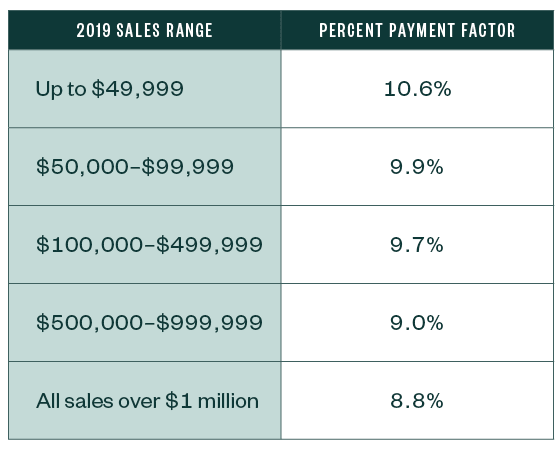

Sales Commodities

Sales Commodities

Sales commodities are specialty crops and livestock that aren’t included under the price trigger category below. These commodities are calculated using a sales-based approach where producers are paid based on five payment gradations associated with their 2019 sales.

Payment rates for sale commodities are reflected in the table below:

Price Trigger Commodities

- Eligible acres multiplied by a payment rate of $15 per acre

- Or, eligible acres multiplied by a nationwide crop marketing percentage, multiplied by a crop-specific payment rate, and then by the producer’s weighted 2020 Actual Production History (APH) approved yield

If the APH isn’t available, 85% of the 2019 Agriculture Risk Coverage-County Option (ARCCO) benchmark yield for that crop will be used.

Payments for Broilers and Eggs

For broilers, payments will be equal to 75% of the producer’s 2019 broiler production multiplied by the payment rate of $1.01 per bird.

Payments for eggs will be equal to 75% of the producer’s 2019 egg production multiplied by the Commodity Credit Corporation (CCC) payment rate.

Payments for Dairy

Dairy payments—specifically cow’s milk—will be equal to the sum of the following:

- Producer’s total actual milk production from April 1, 2020, to August 31, 2020, multiplied by the payment rate of $1.20 per hundredweight

- Producer’s estimated milk production from September 1, 2020, to December 31, 2020, multiplied by a payment rate of $1.20 per hundredweight

FSA will estimate this production based on the producer’s daily average production from April 1, 2020, to August 31, 2020, multiplied by the number of days the dairy operation commercially markets milk from September 1, 2020, through December 31, 2020.

Dairy operations applying for CFAP 2 must be in the business of producing and commercially marketing milk at the time of application.

Dairy operations that dissolve, or have dissolved on or after September 1, 2020, are eligible for a prorated payment for the number of days the dairy operation commercially markets milk from September 1, 2020, through December 31, 2020.

Price Trigger Livestock

Payments are based on a fixed number of head, which is defined as the lower of:

- Highest maximum owned inventory of eligible livestock—excluding breeding stock—on a date selected by the eligible producer from April 16, 2020, through August 31, 2020

- Maximum number of livestock per type established by USDA

Flat-Rate Row Crops

Payments for flat-rate row crops that don’t meet the 5% price decline trigger—or don’t have data available to calculate a price change—will be calculated by multiplying the producer’s share of reported or determined 2020 planted acres of the crop by $15 per acre. This excludes prevented planted and experimental acres.

Eligibility

Eligibility

Producers

Producers of broilers, eggs, and sales commodities who began farming in 2020 and had no 2019 production or sales can’t calculate payments using the methods described above. Payments for these producers will be based on the producer’s actual 2020 production or sales as of the date the producer submits an application for payment.

The following eligibility rules also apply:

- Any individual or legal entity who shares in the risk of producing a commodity may apply for CFAP 2.

- Producers must be in the business of farming at the time of submitting their application to be eligible.

- Contract growers who don’t share in the price risk of production are ineligible.

- Producers can apply for assistance for only commercially produced commodities.

Persons and legal entities also must:

- Comply with the provisions of the Highly Erodible Land and Wetland Conservation Regulations, often called the conservation compliance provisions

- Not have a controlled substance violation

Citizenship

If a person isn’t a US citizen, or resident alien who possesses an I-551 green card, that person must provide a significant contribution of capital, land, and active personal labor to be eligible for CFAP 2.

If a legal entity has more than 10% ownership held by persons who aren’t US citizens or resident aliens, the entity is eligible for payment only if each foreign person in the entity makes a significant contribution of labor to the farming operation.

If the foreign persons don’t make a significant contribution of active personal labor to the farming operation, the legal entity’s payment is reduced by the pro-rata ownership interest held by the foreign persons.

Income

To be eligible for payments, a person or legal entity must have an average adjusted gross income (AGI) of less than $900,000 for tax years 2016, 2017, and 2018.

However, if 75% of their adjusted gross income comes from farming, ranching, or forestry-related activities, the AGI limit of $900,000 doesn’t apply, and the person or legal entity is eligible to receive CFAP 2 payments up to the applicable payment limitation.

Payment Limitations

The total CFAP 2 payment that a person or legal entity may receive, directly or indirectly through attribution of payments, is $250,000. As this is a separate program, this payment limitation is separate from the CFAP 1 payment limit. This limitation applies to the total amount of CFAP 2 payments made with respect to all eligible commodities.

Payment Limitations

The total amount of CFAP 2 payments made to a legal entity—such as a corporation, limited liability corporation (LLC), limited partnership (LP), trust, or estate—is $250,000 unless:

- Two different members of the legal entity each provide at least 400 hours of active personal labor, active personal management, or combination thereof with respect to the production of 2020 commodities—then an entity could receive up to $500,000

- Three different members of the legal entity each provide at least 400 hours of active personal labor, active personal management, or combination thereof with respect to the production of 2020 commodities—then an entity could receive up to $750,000

Although the payment limitation is increased for the corporation, LLC, LP, trust, or estate, each member’s payment limitation remains subject to the $250,000 individual person payment limit whether it’s received directly or indirectly.

These payment limit provisions are different and separate from the payment limitations established by the 2018 Farm Bill.

Ineligible Commodities

Ineligible Commodities

Commodities that aren’t eligible for CFAP 2 include:

- Hay—except alfalfa—and crops intended for grazing

- All equine, animals raised for breeding stock, companion or comfort animals, pets, and animals raised for hunting or game purposes

- Birdsfoot and trefoil, clover, cover crop, fallow, forage soybeans, forage sorghum, gardens both commercial and home, grass, kochia or prostrata, lespedeza, milkweed, mixed forage, pelts excluding mink, perennial peanuts, pollinators, sunn hemp, and vetch

- Seed of ineligible crops

Visit the USDA website for a full list of eligible commodities and more information on CFAP 2 eligibility and payment details related to these commodities.

We're Here to Help

We’re Here to Help

If you have any questions regarding CFAP 2 and your or your company’s eligibility, please contact your Moss Adams professional.

Note on COVID-19

During this unparalleled time, we’re closely monitoring the COVID-19 situation as it evolves so we can provide up-to-date guidance and support to help you combat uncertainty. For regulatory updates, strategies to help cope with subsequent risk, and possible steps to bolster your workforce and organization, please see the following resources:

Shad Winters has practiced public accounting since 2004. He provides taxation, tax planning, and business consulting services for family businesses in the agriculture, manufacturing and distribution, professional services, and not-for-profit industries. He can be reached at shad.winters@mossadams.com or at (559) 835-0195.

Josh Bakke has practiced public accounting since 2010. He focuses primarily on tax consulting and compliance services to agricultural cooperatives, as well as private equity groups that operate in the food and agriculture sectors. He can be reached at josh.bakke@mossadams.com or at (541) 732-3868.

The material appearing in this communication is for informational purposes only and should not be construed as legal, accounting, tax, or investment advice or opinion provided by Moss Adams LLP. This information is not intended to create, and receipt does not constitute, a legal relationship, including, but not limited to, an accountant-client relationship. Although these materials have been prepared by professionals, the user should not substitute these materials for professional services, and should seek advice from an independent advisor before acting on any information presented. Moss Adams LLP assumes no obligation to provide notification of changes in tax laws or other factors that could affect the information provided.

About

Moss Adams LLP has been in business for more than 104 years. The 11th largest accounting and consulting firm in the United States, Moss Adams is the largest headquartered in the West. With more than 27 locations in Washington, Oregon, California, Arizona, New Mexico, Kansas, and Texas, our staff of over 2,600 includes more than 260 partners, we are ready to serve you.

Our Wine Industry Group

Moss Adams’ commitment to providing business solutions to vineyards and wineries of all sizes starts with the professionals who make up our team. Each specialist has proven business and finance expertise coupled with deep knowledge and experience in the wine industry.

We offer a wide variety of accounting, tax, and business consulting services tailored to meet the specific needs of today's wineries and vineyards.

Find out why more than 300 wine industry clients trust our team, from start-up to maturity. We're more than an just an accounting firm to our clients. We're a trusted advisor.

Contact

Contact List

| Title | Name | Phone | Extension | |

|---|---|---|---|---|

| Business Development Executive | Jim Pidgeon | jim.pidgeon@mossadams.com | 415-677-8222 | |

| Wine National Practice Leader | Jeff Gutsch | jeff.gutsch@mossadams.com | 707-535-4109 | |

| Business Development Executive | Ted Grafe | ted.grafe@mossadams.com | 707-535-4146 | |

| Tax Partner | Michael Ricioli | michael.ricioli@mossadams.com | 707-535-4142 |

Location List

| Locations | Address | State | Country | Zip Code |

|---|---|---|---|---|

| Moss Adams x Baker Tilly | 3700 Old Redwood Hwy Ste 200, Santa Rosa | CA | United States of America | 95403 |

List of Locations

Profile Picture