by Steve Fredricks

We are now well past a relatively uneventful and smaller harvest, particularly in the North Coast, mask mandates have been lifted in most areas, and on-premise sales continue to rebound. Overall, the industry seems to be a taking a collective deep breath to assess the current market dynamics, but remains unable to relax totally or look too far ahead.

The market disruptors of Covid-based channel shifting on the consumer side and short crops from drought and fires on the supply side have been exacerbated by geo-political, supply chain, and inflationary issues. The net effect is that supply excesses are down and more in balance to demand. In many ways it feels like the market is more ‘normal’ than it has been for quite some time. At the same time, one must ask: Is this really a return to normalcy, or are we adapting to new normals?

This issue will focus on what we are currently seeing in the bulk wine and grape markets, and will offer an early look at the Southern Hemisphere harvest and how that may impact domestic markets.

Bulk Market Update

by The Bulk Wine Team

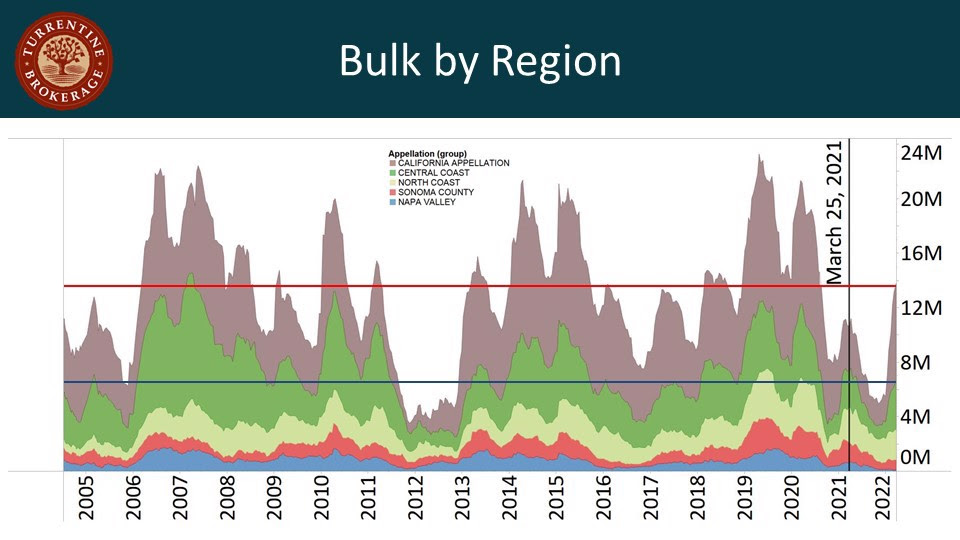

Volume of bulk wine actively for sale in coastal regions appears to have leveled off for the year and remains just below the peak supply from last year. Supply of California Appellation wine is continuing to come to the market, and based on historical trends, it is likely to peak in the near future. Wine becoming available from California Appellation is not a surprise; heading into harvest, the crop was looking short and bulk demand was strong so wineries retained inventory. Meanwhile, slowing retail sales coupled with a somewhat larger-than-expected harvest (albeit still smaller than average) has wineries looking to sell greater volumes than they were listing previously. Statewide, we are currently listing 13.7 million gallons actively for sale, more than we had last year despite a lack of older-vintage lots available.

The bulk market started earlier than usual this year following the 2021 harvest for two reasons: 1) a general tightening of supply following two smaller-than-average harvests, and 2) the lack of older-vintage gallons available.

While interest from buyers started early again this year, there has not been quite the same manic purchasing activity as last year. In recent weeks, we have seen some bulk supply increase to a greater degree than buyers’ needs, but this is not causing too much concern. We will highlight a few continued shortages as we outline some key bullet points to describe the market for top varietals.

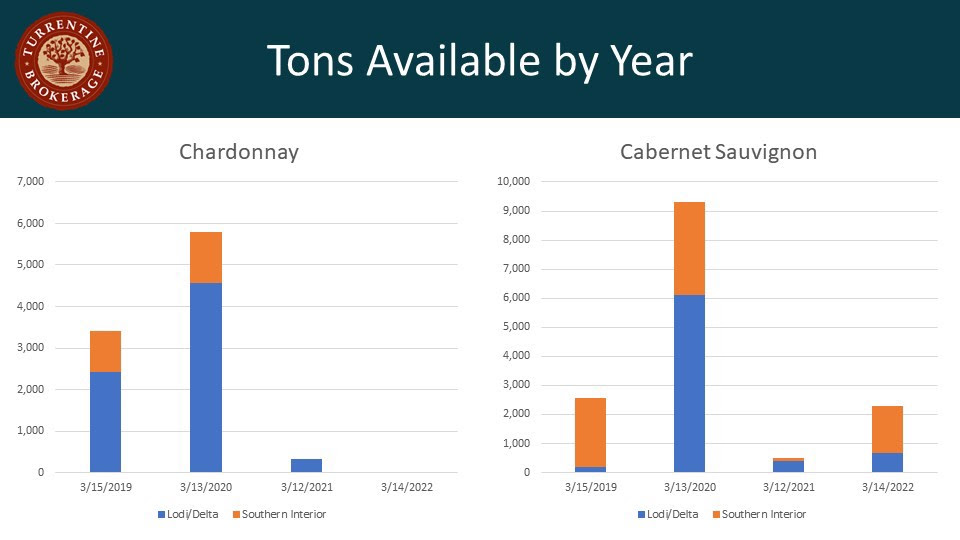

Cabernet Sauvignon

Supply

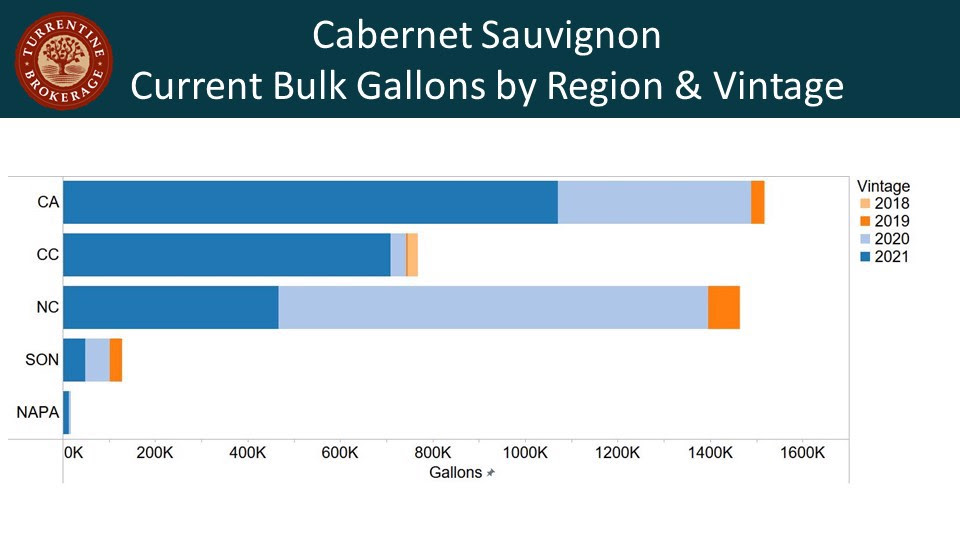

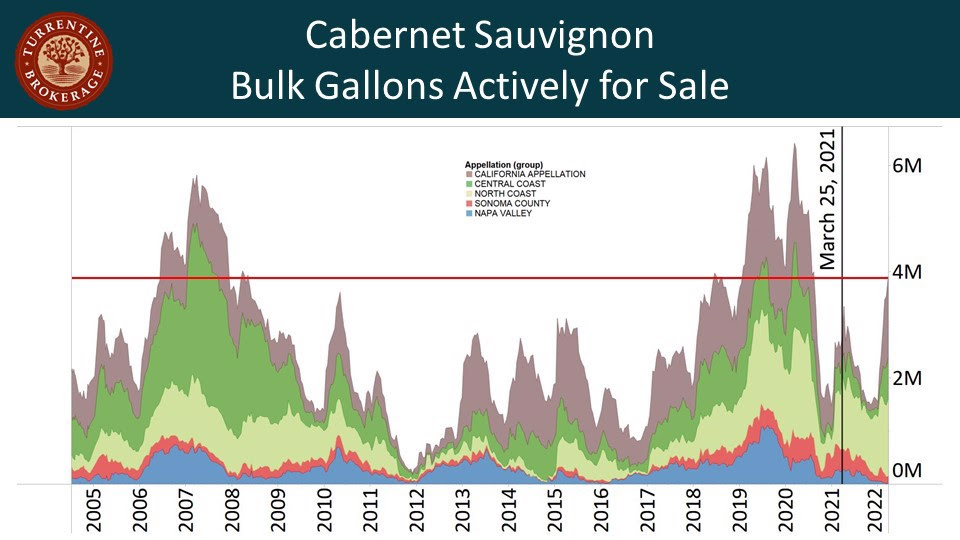

- Total Cabernet Sauvignon bulk supply actively for sale is currently above last year, but still down significantly from the same time in 2019 and 2020.

- More than 25% of the total available bulk wine is Cabernet Sauvignon.

- Significant volumes of North Coast 2020 and 2021 vintage wines are on the market and represent 11% of the total available supply.

- The amount of California Appellation Cabernet Sauvignon is up 300% from the tight supply last year.

- There is extremely limited supply available for 2020 and 2021 Napa Valley wines.

- Supply of 2021 vintage Paso Robles Cabernet Sauvignon has increased, with very few gallons of 2020 vintage wine available.

Demand

- Napa Valley wines continue to be most in demand for Cabernet Sauvignon, with recent prices anywhere from $25.00 to $55.00 per gallon for both 2020 and 2021 vintages.

- We have completed more sales of Sonoma County Cabernet Sauvignon due to a greater availability of supply with recent sales of 2020 and 2021 vintage lots between $24.00 and $30.00 per gallon.

- There continues to be moderate interest for Paso Robles Cabernet Sauvignon, with recent sales between $10.00 to $14.00 and Lodi Cabernet Sauvignon from $7.00 to $9.00 per gallon.

- In general, there is sustained soft demand for North Coast Cabernet Sauvignon lots.

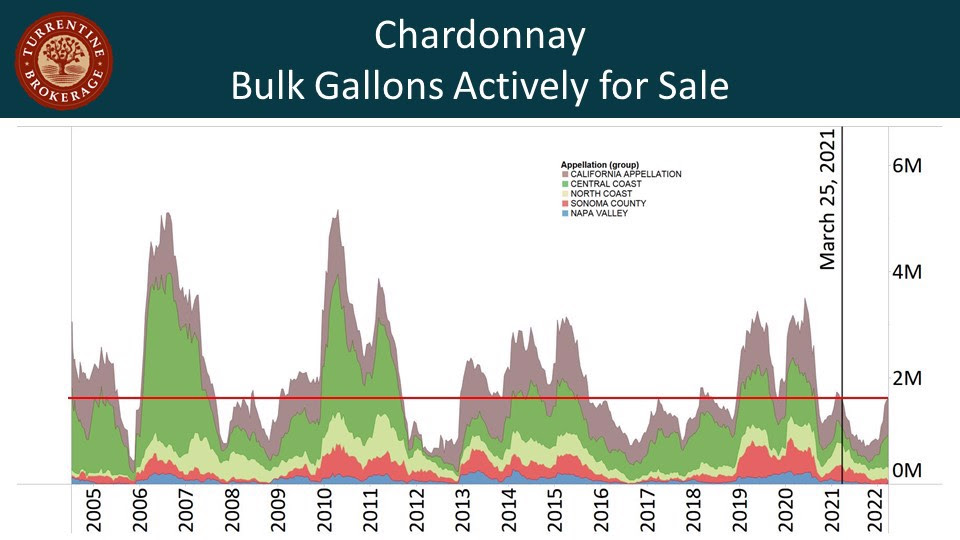

Chardonnay

Supply

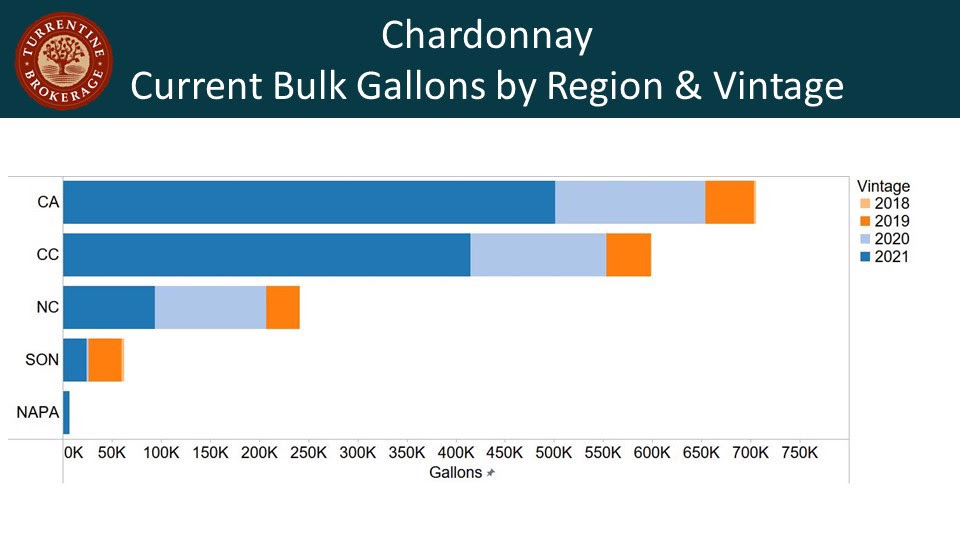

- There is more of a distribution of available bulk Chardonnay gallons than other varieties, both by region and by vintage.

- There are 1 million gallons available of 2021 vintage Chardonnay, with more than 600,000 gallons of 2020 vintage and older vintages still on the market.

- So far in 2022, available gallons are similar to the 2021 totals, both in total volume and volume by region.

- We have continued light supply of Napa Valley Chardonnay.

Demand

- Demand for Chardonnay is moderate and has moved to the 2021 vintage at this point.

- There are more buyers in the market for Chardonnay from Napa Valley and Russian River Valley than anywhere else.

- Demand for 2021 Chardonnay maxes out at $20.00 to $25.00 per gallon, but most buyers are only interested if the price is below $20.00 per gallon.

- There was a decent amount of demand early in the year for Lodi/Delta Chardonnay, but that is starting to stall out as we begin to enter the second quarter.

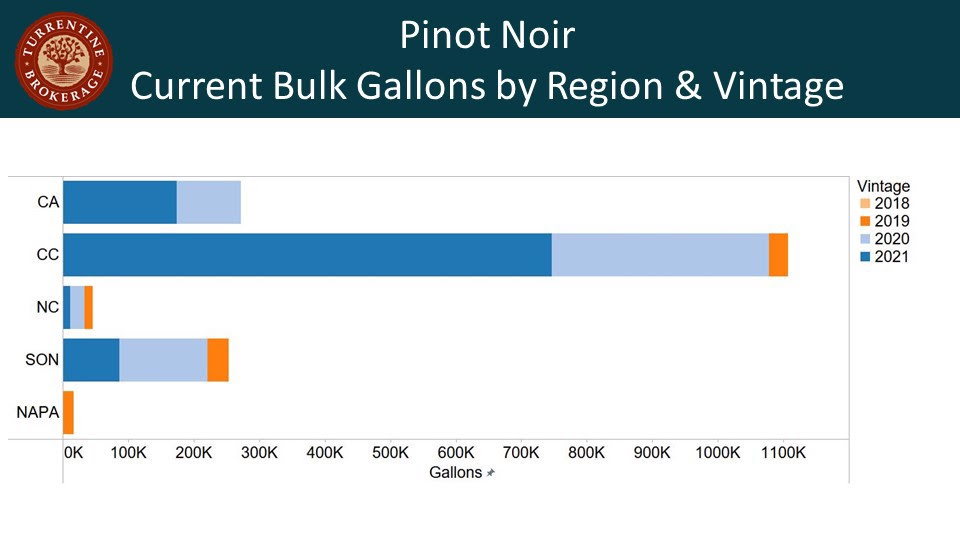

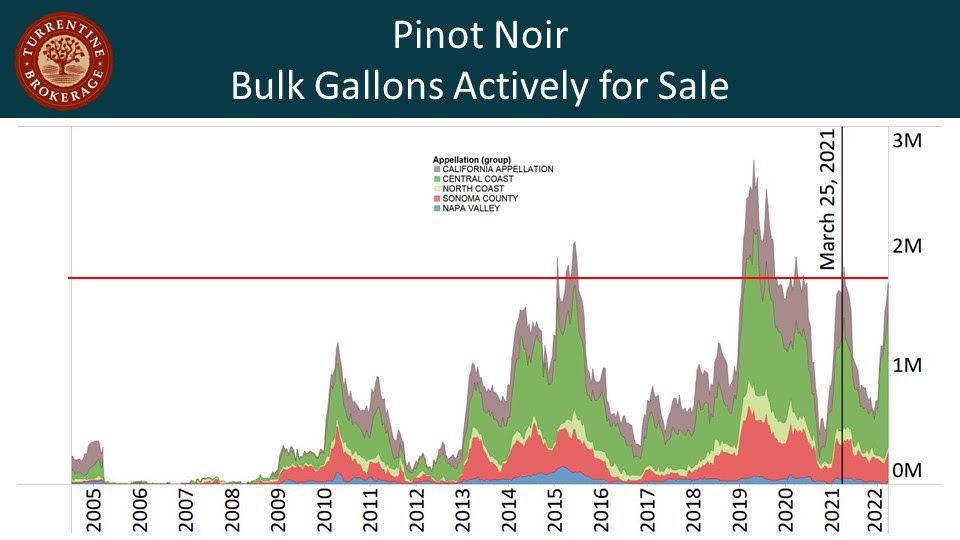

Pinot Noir

Supply

- The majority of Pinot Noir gallons available are from the Central Coast—a region that continues to be in more of an excess position than others.

- There are still a fair amount of 2020 vintage Pinot Noir gallons available.

- Total Pinot Noir gallons are similar to last year, both in total gallons available and by region; but gallons available are lower than in mid-March of 2019 and 2020.

Demand

- Russian River Valley has been the most in-demand region for Pinot Noir, followed by Sonoma Coast, Sonoma County, and Napa Valley with recent sales between $20.00 and $26.00 per gallon.

- The rest of the recent Pinot Noir activity has been for California Appellation between $6.50 and $9.00 per gallon; and demand is softening.

- There is currently little demand for Central Coast Pinot Noir.

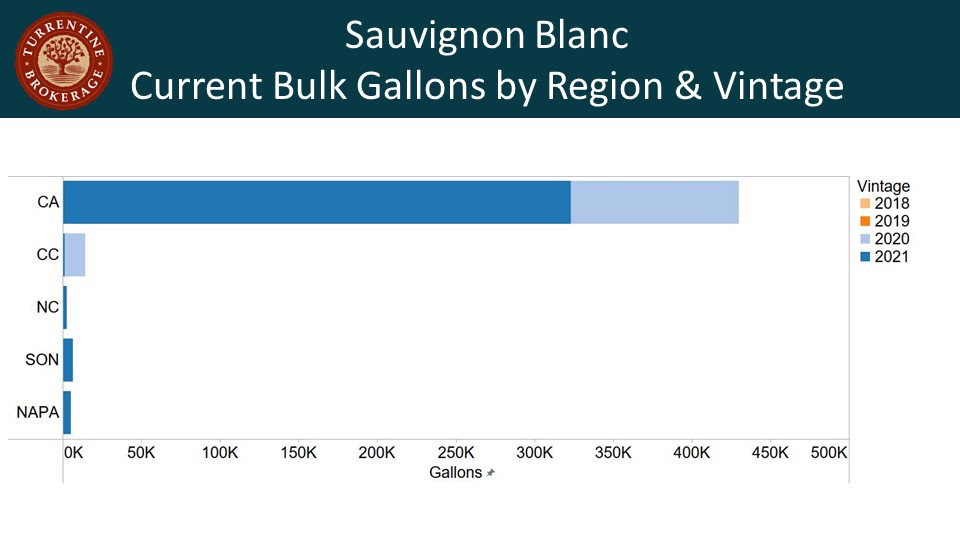

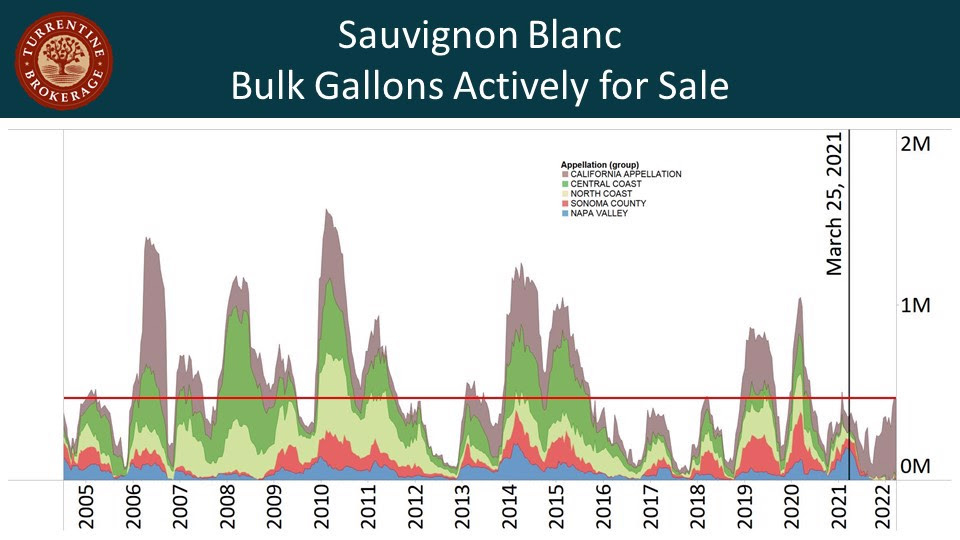

Sauvignon Blanc

Supply

- Virtually all gallons available of Sauvignon Blanc are from the interior due to the larger crop.

- Conversely, the smaller harvest in the North Coast in particular has limited bulk wine available, and there have been a few sporadic listings from coastal regions throughout the year.

Demand

- Buyers are exclusively focused on the 2021 vintage, which limits the more desirable supply to just over 300,000 gallons overall.

- Sauvignon Blanc throughout the coast was very active and has been moving very quickly when available.

- Buyers came in early to purchase California Appellation Sauvignon Blanc to blend into coastal wines.

- Demand for California Appellation Sauvignon Blanc has dissipated from coastal wineries for three reasons:

- Smaller crops in recent years on the North Coast have pushed vintage releases earlier.

- A smaller starting blend means they can only buy smaller volumes to serve as blending components.

- Wineries will need to commit to packaging orders earlier.

- Sales of California Appellation Sauvignon Blanc were between $7.00 and $11.00 per gallon, and recent sales are trending toward the bottom of this range, and likely to continue to decrease.

- The few lots of Sonoma County Sauvignon Blanc that became available have moved between $22.00 and $26.00 per gallon.

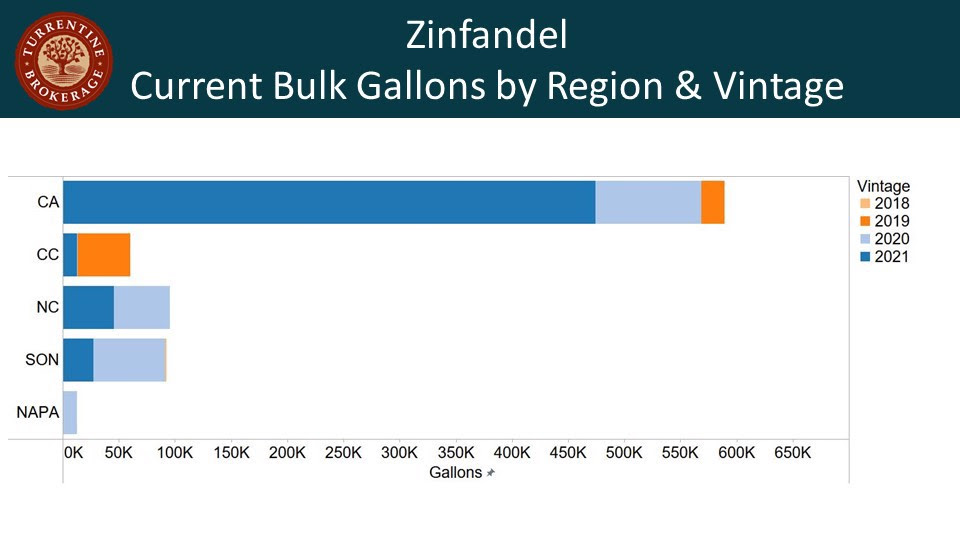

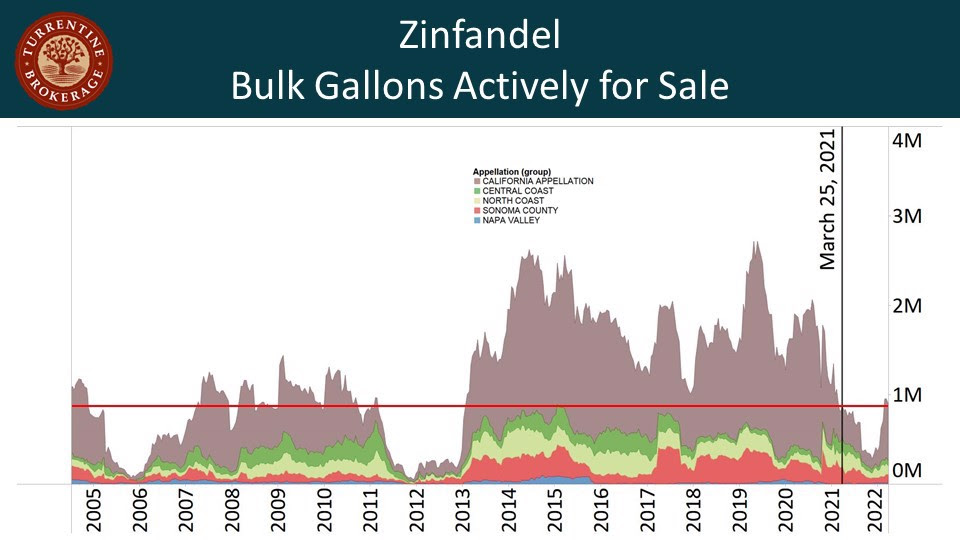

Zinfandel

Supply

- The available supply of Zinfandel in bulk is still heavily weighted towards California Appellation, but the volumes listed are a fraction of what they were from 2014 through 2020.

- There is a significant increase in supply of Lodi Zinfandel available from late last year, when there weren’t any lots available.

- There are very few gallons of 2021 vintage coastal lots available.

- A seasonal peak of 1 million gallons of Zinfandel would be the lowest since 2013.

Demand

- Demand for Zinfandel is driven by buyers looking for Lodi and California Appellation, and the increased volumes for sale present an opportunity for buyers.

- Recent sales of Lodi and California Appellation Zinfandel have been between $7.00 to $8.00 per gallon with moderate to low demand.

- There is limited interest for Zinfandel from the coast.

Grape Market Update

North Coast

By Christian Klier

The grape markets throughout the North Coast have been active early this year, particularly for Napa and Sonoma. This is a likely result of the smaller 2021 harvest paired with what could be a lighter 2022. While there aren’t any indications of cluster counts to this point, the general consensus is that drought conditions could impact potential crop size. Recent isolated frost events in Carneros and Russian River Valley did not help the potential size of the crop for Chardonnay and Pinot Noir.

Wineries have been hedging early, particularly for Cabernet Sauvignon, which has been far more active than this time last year. Still, Cabernet Sauvignon is not the most in-demand variety. That title belongs to Sauvignon Blanc, followed closely by Chardonnay and Pinot Noir.

Central Coast

By Audra Cooper

Wineries were actively re-signing contracts earlier this year, but activity in general has been moderate otherwise. There are still elevated levels of Cabernet Sauvignon available, primarily out of Paso Robles, but there has been purchasing activity as well, so grapes are in motion. Demand also has increased for red blenders, and supply is tighter than it has been in several years for other reds such as Zinfandel, Petite Sirah, Petit Verdot, and Malbec.

Not all markets are moving to the degree of Cabernet Sauvignon and red blenders. Pinot Noir is, in a general sense, still in recovery. There has been sporadic demand for Pinot Noir grapes out of Monterey County and San Benito, but supply still outweighs demand.

Larger-than-expected yields of Monterey Chardonnay last year did not drastically affect the market, but activity did slow down to a degree. So far to this point in the season, activity has been centered around Arroyo Seco and Monterey County.

San Joaquin Valley

By Mike Needham

There are limited grapes out of contract in 2022, which has placed a premium on available supply. A lack of rain since December and the sobering news of partial to no water this year are lowering expectations for growers and wineries alike. Wineries, as a result, are extending contracts with their best growers. As the year progresses, we expect this trend to continue—especially if the crop looks average or below-average and there would likely be upward pressure on grape pricing. Conversely, additional fruit could come to market if the crop looks to be larger, which could place some downward pressure on price, but it is still far too early to predict what might happen at this point.

Wineries are interested in securing supply of all varieties, as there is not a single variety in an excess position currently.

International Update

By Steve Fredricks

Increased costs of shipping, challenges in finding containers, and overall logistical delays are global problems hampering trade of wine. Wineries around the globe are also dealing with inflation in energy prices, increased costs, and challenges in finding glass and packaging—all challenges similar to those facing wineries here at home.

Southern Hemisphere

Argentina

The 2022 harvest season is well underway and the current projections have changed from earlier this season. Leading into harvest, inventories of dry red, dry white, and other varietal whites were below normal. The inventory of Malbec was slightly above normal, but still manageable. Early projections were for normal (long-term average) yields per acre, but as the season has progressed, a number of weather events negatively impacted yields. The early varieties are down 20-30% from long-term averages, and the projections are for Mendoza Malbec to be down in the same range. The net result is that there is likely to be a balanced to short supply of dry red and dry white, and the inventories of Malbec and other varietals will be reduced. There is talk that Argentine wineries may look to Chile for bulk dry red and dry white from 2022. Prices are likely to increase for the 2022 wines compared to the 2021 wines.

Chile

Going into harvest the inventory of Sauvignon Blanc and Chardonnay was well below normal. Bulk prices were very high for any of these available wines. Meanwhile, inventories of Cabernet Sauvignon and Merlot were at normal levels. The 2022 harvest projections are for long-term average yields per acre. Due to low inventory and strong demand, grape prices for 2022 Sauvignon Blanc were higher than or similar to last year. The result is that bulk prices for 2022 Sauvignon Blanc and Chardonnay will be equal to or slightly up from last year. The prices for Cabernet Sauvignon and Merlot are likely to hold steady.

Australia

Leading up to harvest, there was a large inventory of bulk red wine actively for sale as a result of the large 2021 crop and the trade tariff on Australian wines to China. This caused almost all exports to stop, and bulk prices were very low as a result. Costs of shipping containers and the lack of containers available continue to make new and existing deals difficult to complete. Harvest is about halfway complete and yields are down from last year’s highs and down 10-15% from long-term averages, but due to the excess bulk wine and sales challenges, grapes are likely to stay on the vine. All Sauvignon Blanc, Pinot Grigio, and most Chardonnay will be harvested. Most of the red grapes in the high-value regions of Barossa and McClaren Vale will be harvested. Shiraz and Cabernet Sauvignon in the inland areas will most likely stay on the vine. There are some attractive options for wine, but logistics make it more difficult to get deals done. Give us a call if you are interested.

Northern Hemisphere

Europe

The market remains active for wine from the regions that had a light crop in 2021. White wines including Prosecco from Italy, and Sauvignon Blanc and Chardonnay from France are in tight supply. Asking prices increased early after harvest and have been holding steady. So far buyers are meeting sellers’ asking prices. Just as in the United States, inflation, cost of energy and gas, and increased costs of shipping continue to impact business.

The Russian invasion of Ukraine means that generic red, generic white, and entry level varietals may be affected by shipments not going to Russia. Russia is a big market for sweet and flavored sparkling wine from Italy, which will have an impact on those producers, as well. Every market is feeling the challenges of increased costs of fuel, increased costs of transportation, delays in transportation and uncertainty.

Summary

The trend of the supply-to-demand balance for varieties and regions will continue to be mixed. Overall, the market for bulk wine and grapes has been busy again this first quarter. The market is active for Napa Valley and Sonoma County grapes and bulk wine with demand exceeding supply, there is continued growth and recovery of bulk wine and grape demand for Paso Robles Cabernet Sauvignon, and there are opportunities for good Central Coast Chardonnay and Pinot Noir on both the bulk and grape markets. The demand for grapes is strong in the San Joaquin Valley and, with the increased supply of bulk wine, there are additional opportunities for California Appellation 2021 wine.

Circling back to our opening question, the current market is both a return to normalcy and a move toward a new normal. Even though buyers and sellers would like to be making longer-term decisions, the uncertain nature of inflation on all aspects of business, consumer demand, and the uncertainty of 2022 crop size are focusing decisions on short-terms. Since the market is active and opportunities change daily, the strategy for working with us during this time is to contact us as early as possible with your listings or needs for grapes and bulk wine. The more time we have to work with you, the more likely we will be able to provide options and better deals.