Good News & Challenges

The Insurance Market Cycle: Hard Versus Soft Markets

The commercial insurance market is cyclical in nature, fluctuating between hard and soft markets. These cycles affect the availability, terms, and price of commercial insurance, so it’s helpful to know what to expect in both a hard and soft insurance market.

A soft market, which is sometimes called a buyer’s market, is characterized by stable or even lowering premiums, broader terms of coverage, increased capacity, higher available limits of liability, easier access to excess layers of coverage, and competition among insurance carriers for new business.

A hard market, sometimes called a seller’s market, is characterized by increased premium costs for insureds, stricter underwriting criteria, less capacity, restricted terms of coverage, and less competition among insurance carriers for new business.

Recent History – A 2023 Retrospective

Throughout 2023, the commercial insurance space became an increasingly complex environment. There’s been both good news and challenges.

In some lines of coverage—namely, directors and officers’ liability (D&O), employment practices liability (EPL), and workers’ compensation—shifting market dynamics, new capacity, and optimal underwriting results set the stage for improved conditions, which means fewer rate increases and, in some cases, rate decreases.

On the other hand, headwinds facing other coverage segments, such as commercial property and automobile led to diminished profitability and fueled double-digit rate hikes.

Looking ahead, industry experts anticipate that the commercial insurance sector will still carry challenges in 2024; however, it may present more favorable conditions than it has in previous years for some insurance buyers and in certain lines of coverage. Yet, some coverage segments, including commercial property and automobile will likely remain difficult to navigate. Regardless, a proactive approach to risk management in securing adequate coverage will be critical in securing needed insurance during this time. The key will be to address the factors we can control in advance.

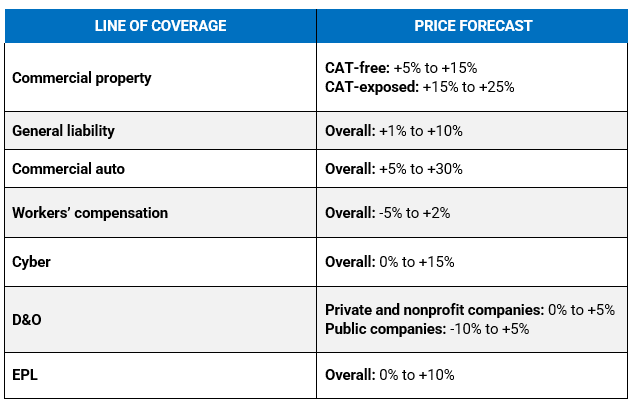

2024 Insurance Rate Forecast Trends

Price forecasts are based on industry reports and surveys for individual lines of insurance. Forecasts are subject to change and are not a guarantee of premium rates. Insurance premiums are determined by a multitude of factors and differ between businesses. Claims history will impact pricing and coverage availability. These forecasts should be viewed as general information, not insurance or legal advice.

Note: CAT refers to “catastrophic perils” such as wildfires, earthquakes, etc.

Your team here at Acrisure is ready to help. While the above predictions are based on expert research, they are subject to change. We encourage you to partner with us to learn price forecasts for your specific business and to set an insurance and risk management strategy that will maximize your protection and minimize cost. Let's have a conversation. Just reply here.