Learn about this common type of business insurance, from the BOP insurance definition to what it typically includes, and more.

Starting a business can involve numerous risks, from financial uncertainties to unexpected liabilities. For entrepreneurs, helping to safeguard your venture against these risks is crucial to ensuring its success. Business insurance can be an essential risk management tool to help manage what could otherwise be a challenging situation. In this article, we’ll tell you about how a common type called BOP insurance works.

What Is BOP Insurance?

BOP insurance, also called a Business Owner's Policy, is a combination of different insurance coverages designed to insure the needs of small to medium-sized businesses.

BOP Insurance Definition

BOP insurance is an insurance policy that combines several coverage types into one policy. A BOP insurance policy typically includes property insurance and liability insurance and can also include business interruption insurance. The goal of a BOP insurance policy is to provide businesses with coverage for common risks they may face, all while offering a cost-effective and convenient solution compared to purchasing each type of insurance separately.

Typical Coverages under BOP Insurance

Commercial General Liability Insurance

Commercial general liability insurance helps protect your business against third-party claims of bodily injury or property damage that occur on the business premises or as a result of its operations. This coverage may be important for businesses that interact with customers, clients, or third parties on a regular basis. It typically helps cover legal fees in the event of a claim as well as resulting settlements or judgments.

Commercial Property Insurance

Commercial property insurance covers the physical assets owned or leased by your business. This may include buildings, equipment, furniture, inventory, and other physical assets essential to the operation of the business. The terms and conditions of each policy may vary but this type of coverage typically protects against losses due to perils such as fire, theft, vandalism, and certain natural disasters.Business Interruption Insurance

Business Interruption Insurance

Business interruption insurance helps cover the loss of income and extra expenses your business may experience if it is unable to operate due to a covered event, such as a fire or natural disaster. This coverage helps businesses financially during the downtime needed for repairs or recovery.

How BOP Insurance Works

When your business requests a quote for a BOP insurance policy, you may be requested to provide certain information such as your industry, size, location, and claims history. These factors will be considered when the insurer issues the quote. If you receive quotes from multiple insurers to compare, you may be able to alter your coverage limits and deductibles to suit your particular needs and to arrive at a price point that works for your budget. Once you secure a BOP, you’ll typically pay a premium on a monthly, quarterly, biannual or annual basis to keep the policy in force (active).

If a covered event occurs, such as a fire damaging your business premises or a customer slipping and falling on the premises, you can file a claim with the insurance company. The insurance company will then assess the claim and, if approved, pay the claim according to the terms of the policy. This payment may cover repairs, replacements, legal costs, and other covered expenses arising from the claim, up to the policy limits (minus any applicable deductible).

Four Benefits of BOP Insurance

1. Cost-Effective Coverage: BOP insurance combines different coverages into one policy, often at a lower premium than purchasing each type of insurance separately. This makes it a cost-effective option for small businesses with limited budgets.

2. More Comprehensive Coverage: BOP insurance is designed to provide broad coverage against many common risks faced by small businesses, offering more peace of mind to business owners who may not have the resources to handle unexpected financial setbacks.

3. Personalized Options: While BOP insurance typically includes standard coverages, businesses can often personalize their policies to add additional coverages specific to their needs. This flexibility allows businesses to personalize their insurance coverage for their specific business needs.

4. Simplified Management: Managing multiple insurance policies can be complex and time-consuming. A BOP helps streamline the process by consolidating coverages into one policy, with the goal of reducing paperwork and administrative burdens for business owners.

What Kinds of Businesses Choose BOP Insurance?

BOP Insurance can be beneficial to many types of businesses. Here are a few examples:

Small-to-Mid Sized Businesses

BOP insurance is popular among small to medium sized enterpr (SMEs) that may not have the resources for extensive risk management strategies but still need comprehensive coverage options.

Retail and Service Businesses

Businesses that interact with customers or clients on their premises, such as retail stores, restaurants, salons, and professional offices, can benefit from liability coverage and property coverage included in a BOP.

Businesses Leasing Space

If your business leases office space or a storefront, property insurance offered under a BOP can help provide financial protection if business property is damaged by a covered event.

Home-Based Businesses

Even home-based businesses can benefit from BOP insurance as, depending on the coverages selected, it can cover business equipment and inventory kept at home and can provide coverage for other business-related risks not typically included in homeowners insurance.

What to Consider When Purchasing BOP Insurance

Before purchasing a BOP insurance policy, it’s important to assess your business's specific needs and risk factors. Consider the following:

Coverage Limits

Ensure the coverage limits of the BOP align with the value of your business assets and potential liabilities. A coverage limit refers to the maximum amount of money that the insurance policy will pay out for a covered claim or loss. It's important for businesses to carefully consider their coverage limits to ensure they have adequate coverage in case of a loss. It's also worth noting that higher coverage limits may result in higher insurance premiums.

Exclusions and Limitations

Review the policy exclusions and limitations carefully to understand what is not covered under the BOP.

Additional Coverages

Determine if you need additional coverages beyond what is included in a typical BOP. Depending on your industry, you may want to add separate policies for additional coverages such as cyber insurance or professional liability insurance.

Insurance Company’s Reputation

Choose an insurance company with a strong reputation for customer service and financial stability. Research customer reviews and ratings to help select a company that has a good reputation for being reliable in the event of a claim.

The Bottom Line

A Business Owner's Policy is a valuable risk management tool to help protect small to medium-sized businesses against financial liability which may arise in the course of doing business. By typically combining commercial property insurance and commercial general liability insurance (with the option of adding other coverages such as business interruption insurance) into one convenient package, BOPs offer comprehensive coverage at a cost-effective price point.

Whether you operate a retail store, a professional office, or a home-based business, a BOP insurance policy can help provide the financial protection and peace of mind you need to focus on growing your business. Assess your business's needs, compare insurance options, and consider consulting with an insurance professional to determine if BOP insurance is the right choice for helping to safeguard your venture's future.

Acrisure’s professionals have BOP insurance expertise. Connect with us to learn more about your BOP insurance options, or request a business owner’s policy quote online now.

Businesses of all sizes can benefit from the protection offered by having business insurance. In this article, learn about different types of business insurance and how to get coverage.

From brick-and-mortar shop owners to online-based businesses, obtaining business insurance to help protect your operations from the unexpected is important. Given the variety of policy options and different insurance companies out there, you may wonder how to find the right business insurance policy for your unique business. If the process feels daunting, we help by breaking down the basics for you here.

Why Consider Business Insurance?

Do you need insurance to run a business? Depending on your business size and type, certain state and/or federal requirements may mandate that you secure certain insurance coverages for your business. Moreover, certain contractual obligations (e.g. customer agreements, loan requirements) may necessitate you obtain and maintain insurance for your business.

While business owners may seek to structure their business in a certain way to help protect personal assets, for example creating an LLC or corporation, business insurance helps protect the assets of the business.

What is business insurance for?

Business insurance can help protect businesses from certain losses and liabilities that may arise when running a business. It can be an important risk management tool, helping to navigate what could otherwise be a challenging situation. Depending on the type of coverage purchased, business insurance generally helps protect businesses from financial losses due to certain covered events, which may be unexpected. Depending on the business's unique needs and the coverages selected, business insurance can help cover claims resulting from:

- Property damage

- Professional errors

- Natural disasters

- Bodily injuries

Lawsuits and settlements can be costly. Unfortunately, some businesses may end up closing their doors if they are forced to pay for claims out of pocket, for example. Business insurance can help provide financial protection in such situations.

Determine What Types of Insurance You May Need

Some business insurance coverage types may be statutorily required. For instance, most states require employers to maintain workers' compensation insurance. Always be sure to check regulatory requirements when shopping for business insurance options. Next, consider your business’s level of risks.

Analyze Your Risks

Each business may have unique risks to consider. For example, if you practice law, you may have a higher chance of facing legal malpractice claims. Also, consider the types of accidents that may happen at your location. For instance, claims resulting from slip-and-fall accidents may be more common if you own a brick-and-mortar shop.

Choose Insurance Coverages Based on Your Business Needs

There are many different types of business insurance policies to consider. They each provide coverage for different types of claims and losses. Some of the most common types of business insurance include the following:

(Note the terms, conditions and exclusions of each policy will vary but the following provides a general description of what is typically covered)

Commercial General Liability Insurance

Commercial general liability insurance (CGL) is a common coverage choice for businesses of all sizes. A CGL policy generally covers third party bodily injury and property damage claims and may also cover claims related to slander and libel. CGL policies typically do not cover damages to the business’s own property or bodily injury suffered by the business owner or its employees.

Commercial Property Insurance

Commercial property insurance is a type of insurance designed to help business owners protect the value of a covered building and its contents (such as furniture, equipment) and exterior fixtures features (such as fences) against covered losses. A commercial property insurance policy will typically cover such losses resulting from certain events including, for example, fires, windstorms and vandalism. A business owner can obtain a standalone commercial property insurance; however, commercial property insurance coverage may also be available under a Business Owner’s Policy, discussed below.

Business Owner's Policy (BOP)

Business owners may enjoy the convenience of a business owner’s policy, which typically combines commercial general liability insurance and commercial property insurance into one policy. Obtaining a BOP can help reduce costs and may simplify the buying process.

Workers’ Compensation Insurance

Workers' compensation insurance typically provides coverage for employees who are injured or become ill as a result of their employment, including medical expenses and lost wages. This type of coverage may be required by state law so it is important to understand the workers’ compensation laws in the state where the business resides.

Professional Liability Insurance

Businesses that provide professional services should consider professional liability insurance. Professional liability insurance typically covers claims alleging negligence and malpractice.

Cyber Insurance

Cyber insurance helps protect businesses against financial liability arising from data breaches, cyber attacks, and other cyber-related incidents. It typically covers expenses such as legal fees, notification costs, and customer compensation.

Commercial Auto Insurance

Commercial auto insurance provides coverage for vehicles used for business purposes and may include, for example, collision, liability, comprehensive, personal injury, medical payments, and uninsured/underinsured motorist coverages.

Product Liability Insurance

Product liability insurance helps protect businesses from financial liability that may arise from claims alleging that defective products they manufactured or sold caused harm, injury or other damages to consumers. It typically covers expenses such as legal defense costs, settlements, and judgments.

How to Get Business Insurance

Know The Basic Steps: Purchasing business insurance involves a few basic steps. After analyzing your risks and identifying potential business insurance types which may work for your needs, you should research insurance companies or start working with a broker. You’ll need to provide details about your business in order to request quotes and then you'll be able to review coverage options. When you have identified policies that satisfy your specific needs, you can secure the coverage.

Shop Around for Quotes: Before you choose an insurance company to issue the policy, shop around for quotes from different insurers. When comparing the quotes, try to avoid just comparing the costs, as less expensive options may provide less coverage. Instead, try to also compare coverages, limits, premiums, payment terms and the insurance company’s reputation. In many cases, you can request business insurance quotes online.

Try Using a Broker: Using the services of an insurance broker can be beneficial as a broker can represent your interests and needs. The broker will have a conversation with you about your business's needs before providing you with available coverage options. You may have access to a wider network of insurers when you work with a broker and you will have someone with real expertise working in your corner.

Purchase Your Policies: Once you narrow your available coverage options, you can make the decision to proceed with purchasing the policy or policies which meet your company's needs. Make sure you mark down when monthly payments are due as well as any renewal dates. You should reevaluate your coverage as your business changes and grows.

Help Protect Your Business with Acrisure

Now that you know the basics of how to get business insurance, you may be considering adding coverage. Request a business insurance quote online today or contact us to discuss other policy options that may be right for your business.

In this article, we discuss the importance of helping to protect a business's senior management team and the company itself with management liability insurance.

Management liability insurance is a combination of different types of coverages which can help protect businesses against the unique risks faced by their organizations and senior management teams. This type of coverage is designed to help protect the company and its executives from certain claims arising in the course of business—for example, mismanagement, negligence, breach of fiduciary duties, harassment, etc.

Management liability insurance has become an important safeguard. It helps protect the organization's sustainability and can offer personal liability protection for its leaders. For any entity navigating the complexities of the corporate world, understanding and securing management liability insurance is both prudent and strategically sound.

Four Key Components of Management Liability Insurance

Management liability insurance typically includes any of the following four coverages:

Directors & Officers (D&O) Liability Insurance: This coverage helps protect the personal assets of directors and officers from lawsuits alleging wrongful acts in their managerial capacities. It typically covers legal fees, settlements, and other defense costs.

Employment Practices Liability Insurance (EPLI): This coverage helps provide financial protection against claims from employees alleging violations of their legal rights, such as wrongful termination, discrimination, or harassment.

Fiduciary Liability Insurance: This coverage typically covers claims alleging a breach of fiduciary duties, which can occur when managing employee benefit plans. It helps protect against claims of mismanagement and the failure to act in the best interests of the beneficiaries of these plans.

Crime Insurance: Crime insurance coverage helps protect the organization from losses due to crimes like fraud, theft, or embezzlement.

The Importance of Management Liability Insurance

In the dynamic and often unpredictable world of business, management liability insurance can help protect organizations and senior management against some of the risks inherent in managing a company.

Protection Against Liability

One of the primary benefits of management liability insurance is its role in helping to protect against financial liability arising from certain lawsuits or claims. Business leaders routinely make decisions that could potentially lead to financial liability. In such scenarios, management liability insurance becomes an important risk management tool for both the individual and the organization as a whole.

Potential Scenarios Demonstrating the Importance of Management Liability Insurance

Lawsuits for Alleged Mismanagement: Directors and officers may face lawsuits alleging mismanagement or negligence in the performance of their duties for others. These lawsuits could come from shareholders, employees, competitors, or regulators, for example. Management liability insurance helps cover the legal costs associated with the defense or settlement of such claims, helping to protect both the personal assets of these individuals as well as the financial stability of the organization.

Employee Claims: A company may face allegations such as wrongful termination, discrimination, or harassment from its employees. EPLI coverage can help protect a company against the legal costs and potential damages arising from such claims.

Fiduciary Claims: Fiduciary liability insurance may be important for companies managing employee benefits and retirement plans. Claims of mismanagement or negligence against those who act as fiduciaries can present unique challenges. Fiduciary liability insurance can help protect against the financial liability associated with such claims.

Crime-Related Losses: Crime insurance helps protect a company against financial losses associated with business-related crimes such as fraud, embezzlement, or theft.

Management Liability for Different Organizations

Management liability insurance is not a one-size-fits-all solution; its relevance and structure can vary significantly across different types of organizations. Private companies, nonprofits, and publicly traded companies each have unique risk profiles and, therefore, may require tailored approaches to management liability coverage.

Private Companies: In private companies, including small and medium-sized businesses, the personal assets of directors and officers can be at risk. These leaders may make decisions that could potentially expose them to lawsuits from employees, clients, or other parties. Management liability insurance for private companies typically focuses on helping to provide protection for the personal assets of these individuals against such third-party claims and covering the potential legal and financial liabilities of the company itself.

Nonprofit Organizations: Nonprofit organizations may have different operating dynamics, often with boards consisting of volunteers who might not be aware of the extent of their legal responsibilities. The potential claims against these organizations may include employment practices liabilities, breach of fiduciary duties, and potential lawsuits from donors or beneficiaries. Management liability insurance for nonprofits is crucial in helping to protect the personal assets of board members and the organization's financial stability.

Publicly Traded Companies: Publicly traded companies face unique challenges due to their exposure to shareholder lawsuits, regulatory scrutiny, and the complexities of compliance with various laws and regulations. These companies may seek management liability insurance options that cover directors and officers against claims from shareholders, regulatory bodies, and other external entities. The insurance policy should be broad enough to address the heightened risks associated with public trading.

Choosing the Right Management Liability Insurance

Selecting the appropriate management liability insurance coverage is an important decision for businesses and organizations. This process involves understanding your business's specific needs, evaluating various insurance policy options, and choosing a reliable insurer. Here are some tips to help guide you through this process.

Understanding Your Business Needs

Assess Your Risk Profile: Different organizations face varying levels of risk. Consider factors like your industry, company size, and the nature of your business operations to help assess your risk exposure.

Identify Key Areas of Coverage: Depending on the nature of your organization, you may need enhanced coverage options in certain areas such as D&O liability, EPLI, or fiduciary liability.

Evaluating Policies and Insurers

Compare Coverage Options: Review different policies to see what is offered under each. Pay close attention to coverage limits, deductibles, exclusions, and any specific conditions.

Check Insurer Reliability: Research insurers to ensure they are financially stable and have a good reputation for handling claims.

Understand Policy Terms: Carefully read the policy’s terms to understand what is covered and what is not under each specific coverage offered.

The Role of Insurance Brokers and Agents

Insurance brokers and agents can bring an advantage when researching management liability insurance options. They can provide valuable insights into the types of management liability insurance that may be best suited for your particular business and, based on their industry expertise, may be able to analyze your needs and recommend the best coverage options available. It is helpful to understand the difference between insurance brokers and agents. One difference is that brokers represent you and can compare policies from different insurers, while agents represent specific insurance companies.

Be clear about your business needs and concerns when consulting with a broker or agent. This helps enable them to provide the most relevant and accurate advice.

Acrisure's expertise in management liability insurance can be instrumental in guiding you through the management liability insurance policy selection process. Our business insurance professionals and employee benefits solutions teams can help you compare policies so you can get the right coverage for your organization's risk profile and objectives.

Contact us today.

Having workers' compensation insurance in place is an important employer practice. In this article, we tell you how workers' comp works and how it might be important for your business.

When employees come to work, they can expect to be in a safe environment. But sometimes despite an employer’s best efforts, unexpected injury or illness can happen. When something does happen, employers can rely on workers' compensation insurance to protect their business and their employees. Workers' compensation or workers' comp is an important part of running a business and protecting workers and companies. But how does workers' compensation work?

Read on to learn more about how workers' comp works from Acrisure. We have expertise in workers’ compensation insurance and can help guide you through the ins and outs of this important policy.

What Is Workers' Compensation?

Workers' compensation insurance or workers' comp helps provide financial and medical benefits to an employee who is sick or injured from a work-related accident or illness. This insurance pays for the covered medical bills and lost wages of the employee as they recover from the accident or illness. If an employee dies from a work-related accident, workers' comp insurance helps provide payments to the employee's beneficiaries.

Workers' comp is a "no fault" type of insurance program. That means that it doesn’t' matter who was at fault for an incident to determine coverage. Anyone involved, so long as the incident took place as part of the work environment, could receive full workers' comp coverage. To receive coverage, an employee must show that the injury or illness came from their place of employment.

Workers' comp is required by law in many states because of the protection it provides and the benefits for both employees and employers. Some states will even require companies to carry this insurance as soon as the first employee is hired. Even if workers' compensation isn't required by law in a state, it is always beneficial to provide coverage.

What Is Typically Covered by Workers' Compensation?

Workers' comp helps provide coverage for injuries and illnesses sustained from something related to work. These are some of the things a workers' comp program would typically cover:

- Carpal tunnel

- Back injuries from repetitive movement or lifting heavy objects

- Injury to the lungs from breathing toxic substances

- Slip and falls while at the workplace or doing something for work

- Injuries sustained in a car accident while driving for business

- Severe injuries from things like electrocution that happened while at work or on the job

These are some injuries that workers' comp typically doesn't cover:

- Injuries sustained while under the influence of alcohol or drugs (proven with blood/alcohol tests

- Self-inflicted injuries

- Injuries sustained while the employee was violating a law or company policy

- Injuries from accidents during the commute to or from work

Who Benefits from Workers' Compensation?

Workers' compensation insurance may be required by law, but it’s for good reason. Workers' comp helps provide protection and benefits to both employees and the employer, so everyone has some protection.

Workers' Compensation Benefits for Employees

A work-related injury or illness can be physically, emotionally, and financially disastrous for an employee. While employers can't always provide for some of the damage, they can help provide financial compensation that will help ease the burdens of a work-related injury or illness with workers’ comp. These are some of the key benefits of workers' comp for employees:

- Covers paychecks missed due to the injury or illness. Covering these expenses eases much of the burden of missing work to recover.

- Helps cover the medical bills from the injury or illness. Medical bills can be extensive and put extreme strain on an injured or sick employee and their family, so help with covering these expenses is a major benefit of workers' comp.

- Helps protects the employee's job while they recover. Employees can recover without having to worry that they won't be able to return to work when they've recovered.

- Helps provide a beneficiary benefit. If an employee is killed on the job, their family will be provided with a beneficiary benefit that will help cover many costs.

Workers' Compensation Benefits for Employers

Workers' comp doesn't just protect employees; it helps protect the employers as well. Essentially, if an employee is injured in a work-related incident, the employer could be legally responsible for providing compensation. This insurance policy is what makes providing that compensation affordable and possible. These are some of the key benefits of workers' comp for employers:

- Helps cover compensation for employees. Without the insurance policy covering the compensation, employers would typically need to cover some of it out-of-pocket. Medical bills and missed paychecks ad up quickly, and employers can struggle to provide these checks without the insurance policy.

- Helps cover legal fees if necessary. If an employee sues the company for the injury or illness they sustained at the company, workers' comp insurance can help cover the employer's legal needs as part of employer's liability insurance. This part of workers' comp could cover legal fees, settlements, and judgements, so the employer doesn't have to pay out-of-pocket.

- Helps companies meet legal requirements. Workers' comp is required by law in many states, so providing it helps a company meet legal requirements.

- Helps protect businesses from lawsuits and going under. A company is less likely to be sued by an employee if the employee is provided workers' comp. In addition, paying for lawsuits or for employee medical bills and paychecks can cause businesses, especially small businesses, to go under due to the financial distress. Protecting employees helps protect employers.

Who Pays for Workers' Comp?

Since both employers and employees benefit from workers' comp insurance, it can be confusing to know who pays for workers' comp. Even though workers' comp does provide major benefits for employees, they aren't required to pay any of the insurance premiums to benefit. Instead, workers' comp insurance is paid for by the employer. The employer pays workers' comp insurance premiums both to adhere with legal requirements and in exchange for the protection this insurance program provides.

Workplace Safety

While workers' comp insurance is beneficial, it should be viewed as a failsafe and only have to be used for rare accidents. Figuring out how to file for workers' comp and all of the complexities can be time consuming to have to do over and over again. Instead, employers should focus on improving workplace safety to reduce the number of workers' comp claims and to keep their employees safe. These are some ways to improve workplace safety:

- Hold regular safety training. Safety training meetings and programs can be a good way to reinforce safety protocols, teach employees how to handle equipment safely, and provide guidance on protecting themselves from repeated motion strain injuries.

- Improve signage. Clear labels and signs can help improve worker safety and prevent injuries.

- Encourage stretch breaks. Having employees stretch and take breaks from repetitive tasks and motions can help prevent some workplace injuries.

- Consult an occupational health expert. If a company is unsure of how to improve safety in a particular area or environment, occupational health experts can be a great resource. They can help guide companies to include the right policies and training practices. They can identify high risks for injury and help companies take the right prevention steps.

- Keep the workplace clean. A clean workplace is one where accidents are simply less likely. Cleaning spills and leaks can help prevent slips and falls while avoiding tangled cords can help prevent trips and dangerous electrical accidents.

The Bottom Line

Overall, workers' comp insurance helps provide coverage for workplace injuries and illnesses. Workers benefit as they can typically have their medical care and paychecks covered by this policy type. Employers also benefit as they will be more protected from legal ramifications, extensive out-of-pocket costs, and potential business losses. Employers pay for this insurance policy and can also endeavor to take care to improve workplace safety as a preventive measure.

Workers' comp insurance is important and valuable. If you want to know how to get workers' comp insurance, Acrisure can help. Request a workers’ compensation insurance quote online today to get started providing workers' comp for your employees and to protect your business, or contact us to learn more.

Life insurance policies can help serve as a financial safety net, providing your loved ones with financial support in the event of your passing. But did you know that life insurance can also be a valuable source of funds during your lifetime? In this guide, we'll explore the concept of borrowing from life insurance policies, shedding light on key aspects to be aware of in order to make informed decisions.

Life insurance policies can help serve as a financial safety net, providing your loved ones with financial support in the event of your passing. But did you know that life insurance can also be a valuable source of funds during your lifetime? In this guide, we'll explore the concept of borrowing from life insurance policies, shedding light on key aspects to be aware of in order to make informed decisions.

Borrowing from a life insurance policy involves accessing the funds that have accumulated over time within the policy. These funds are often called the "cash value" of a policy. While the primary purpose of life insurance is to provide a death benefit to specified beneficiaries, certain policies allow the policyholder to tap into this cash value while they are still alive.

The Concept of Cash Value in Life Insurance

The cash value of a life insurance policy is the amount of money that has accumulated within the policy over time. This cash value can be considered a savings component and may be invested by the insurance company. Policyholders may be able to borrow against the cash value of some life insurance policy types, effectively using their policy as collateral for the loan.

Eligibility for Borrowing from Life Insurance

First, it is essential to understand which policy types may accumulate cash value. The question becomes whether a policy is a permanent life insurance type that provides coverage for the entire lifetime of the insured or if the life insurance policy is a temporary type that provides coverage for a specific term, such as 10 or 20 years.

Permanent vs. Term Life Insurance

1. Whole Life Insurance Policies

Whole life insurance policies are a type of permanent life insurance that builds cash value over time. Borrowing against a whole life policy is typically straightforward, as it accumulates cash value consistently throughout the life of the policy.

2. Universal Life Insurance Policies

Universal life insurance policies are another type of permanent life insurance and generally offer more flexibility in premium payments and death benefits. They also build cash value, which policyholders may be able to access through loans. However, cash value growth in universal life policies may vary based on factors such as interest rates and market performance.

3. Term Life Insurance Policies

A term life insurance policy is not a permanent type of life insurance because it only provides coverage for a specific term of the insured's life. Term life insurance policies do not build cash value. The premiums paid for term life insurance go towards the cost of providing life insurance coverage for that term and do not accumulate as cash value.However, some term policies offer the option to convert to permanent life insurance, such as whole or universal life. Once converted, the policy may accrue cash value that can be borrowed against.

Understanding Policy Values

Next, knowing more about the different kinds of value associated with life insurance policies is important.

Face Value, Death Benefit, and Cash Value

Life insurance policies can refer to the policy's value in different ways, such as:

- Face Value: The amount the designated beneficiaries will receive upon the insured's death.

- Death Benefit: Synonymous with the face value, this represents the payout to beneficiaries.

- Cash Value: The cash value is the amount of money available for borrowing or withdrawal. It grows over time as premiums are paid and may be influenced by the performance of the investments made by the insurance company, depending on the policy type.

Some policyholders believe that borrowing against the cash value will reduce the death benefit. However, borrowing against the cash value typically does not impact the death benefit, provided the loan is repaid. On the other hand, outstanding loans at the time of the insured's passing will be deducted from the death benefit paid to the beneficiaries.

The growth rates of cash value can vary significantly based on the type of policy and the insurer's investment performance. It is essential to review the policy's annual statements to track the growth of the cash value and evaluate whether it meets financial goals.

How Life Insurance Loans Work

It is important to understand how life insurance loans work before planning to take out such a loan. Here are some tips:

Process and Ease of Obtaining a Loan

Obtaining a loan from a life insurance policy doesn’t have to be a complicated process. The loan can be requested through the insurer and is typically secured by the cash value of the policy. Typically, no hard credit check is required, potentially making it an accessible source of funds.

Tax Implications and IRS Recognition

Life insurance policy loans are generally not considered taxable income by the IRS. This means income tax will not be owed on the borrowed funds. However, it's crucial to understand that if the loan is not repaid and the policy lapses or terminates, the outstanding loan balance may be subject to taxation.

Impact of Policy Loans on Cash Value and Death Benefit

When money is borrowed from a life insurance policy, the loan amount is deducted from the cash value. The cash value can continue to grow, but at a reduced rate, as it may take time to recoup the borrowed amount. Additionally, any unpaid loans and accumulated interest will be deducted from the death benefit upon the insured’s passing.

Repaying a Life Insurance Loan

Repaying a life insurance loan is a common concern. Consider the following:

Importance of Timely Repayment

Timely repayment of the loan is essential to maintain the financial integrity of a life insurance policy. Failing to repay the loan and interest can lead to undesirable consequences, such as policy lapse or reduced death benefit.

The Compounding Nature of Loan Interest

Interest on life insurance policy loans is typically lower than that of traditional loans. However, it's important to note that the interest compounds over time. As such, the longer it takes to repay the loan, the more interest will accrue.

Consequences of Loan Default

If the outstanding loan balance, including accrued interest, exceeds the cash value of the policy, the policy may lapse. In such cases, the insured could lose coverage, and the policy's financial benefits would no longer be available to them or their beneficiaries.

Effect of Unpaid Loans on Death Benefits

In the event of the insured's passing with an outstanding loan balance, the unpaid loans and accrued interest will be deducted from the death benefit paid to their beneficiaries. Depending on the amount of the loan and accrued interest, this can significantly reduce the benefit amount paid by the policy to their loved ones.

Potential Pitfalls of Borrowing from Life Insurance

Reduction in Death Benefit

Borrowing from a life insurance policy can reduce the death benefit paid to the beneficiaries if the loan is not repaid before the insured passes.

Risk to Policy Guarantees

Some life insurance policies have specific guarantees, such as a guaranteed minimum death benefit or cash value growth rate. Borrowing against the policy can jeopardize these guarantees, potentially altering the policy's original terms.

Additional Premium Costs

If a policy lapses due to unpaid loans or other reasons, reinstating the policy may come with additional premium costs. These costs can be higher than previous premium payments.

Borrowing Limits and Timelines

The amount that can be borrowed from a life insurance policy is typically determined by the cash value accumulated within the policy. Insurers often have established guidelines regarding borrowing limits, which may be a percentage of the cash value.

A policy loan can generally be requested at any time once the policy has accumulated sufficient cash value. While there is typically no strict timeline for borrowing, it's essential to consider financial needs and goals when deciding when to access a policy's cash value.

Specifics of Borrowing Against Different Policies

Whole life insurance policies are generally a good choice for borrowing against due to their consistent cash value growth. These policies can typically offer a stable source of funds and can serve as a financial safety net.

Universal life insurance policies may offer flexibility in premium payments and death benefits. Borrowing against these policies can be advantageous, but the growth of cash value may be subject to market fluctuations.

The Bottom Line

Borrowing from a life insurance policy can be a useful source of monetary funds. It can come with several advantages, including accessibility, and such loans typically do not require hard credit checks.

While life insurance policy loans can be a valuable financial tool, they come with responsibilities. It's essential to consider how a loan might impact the ultimate payable benefit and a plan to repay the loan should be developed. Insurance advisors or agents can be consulted for personalized guidance on borrowing from a life insurance policy.

If you have questions about borrowing from your life insurance policy or need assistance with your life insurance needs, Acrisure is here to help. Our life insurance policy experts can work closely with you, taking into account your unique needs and financial objectives. As independent life insurance brokers, we offer advice and can provide access to different insurance policy options from a variety of insurance companies. Contact us today or request a life insurance quote online now.

Life insurance is a type of insurance policy where, in exchange for the payment of premiums, the insurance company will provide the insured’s designated beneficiaries a financial benefit upon the insured’s death. This benefit can be used to help cover expenses such as funeral/burial costs and medical bills. It can also be a source of financial security for loved ones and dependents.

Common Types of Life Insurance

The two most common types of life insurance policies are term life insurance and permanent life insurance.

Term life insurance is a policy that provides coverage for a specific term or time period of the policyholder’s life, typically 10-30 years. Beneficiaries receive a death benefit if the policyholder passes away during the term of the policy; however, if the policyholder outlives the term, the coverage ends (unless the policy is renewed or converted).

A permanent life insurance policy covers the policyholder’s entire life, features fixed premiums and a guaranteed death benefit, along with a savings component that grows over time. The cash value of a whole life insurance policy can be borrowed against or even withdrawn lifetime of the policyholder as long as premiums are paid.

Choosing the right life insurance policy is important. The decision not only considers the appropriate financial protection for loved ones, but other factors such as pricing, rates, duration and policy type should be explored as well. That’s why many people turn to a life insurance broker to help find the policy that is right for them. But what is a life insurance broker? Read on to learn about life insurance brokers, the difference between an agent and a broker and the benefits of using a broker.

What Is a Life Insurance Broker?

A life insurance broker helps customers and clients find the right insurance coverage for their specific needs and circumstances. Since brokers are not typically employed by an insurance company, they can offer policy options from several different insurers and use their expertise to help find the right insurance coverage options and rates.

There are generally two types of life insurance brokers: traditional brokers and online brokers. Traditional brokers will typically meet with their clients in person and walk them through the entire process of buying life insurance. An online broker, on the other hand, will offer virtual life insurance policy quotes and rate comparisons. Making the choice between a traditional broker and an online broker will depend largely on the customer’s goals.

If the goal of using a broker is to learn more about insurance options and discuss policy types, a traditional broker may be the right choice. If, however, the customer has already decided on a policy type and just wants to compare rates, an online broker can be a great option.

Life Insurance Broker vs. Life Insurance Agent

When shopping for insurance, it may be common to hear the terms "insurance agent" and "insurance broker." While these terms are sometimes used interchangeably, they actually have different meanings within the insurance market. Both insurance brokers and insurance agents are required to maintain a state license and both can help make buying insurance easier. One of the key differences, however, is who they work for - insurance agents generally represent insurance companies while insurance brokers represent buyers.

There are two common types of insurance agents: captive and independent. A captive agent works for one insurance company and can only sell insurance on behalf of that company. An independent agent, on the other hand, can work with and sell insurance on behalf of multiple insurance companies. Ultimately, since insurance brokers do not have a contractual obligation to any one insurance company, they may have more flexibility in helping to find the best policy for their clients’ specific needs and may be able to offer more competitive pricing options.

How Does an Insurance Broker Make Money?

If a life insurance broker isn’t employed by an insurance company, how do they make money? The answer can depend on the state a broker is licensed in, but in general, insurance brokers typically make money on commission. When a policyholder purchases a life insurance policy, the broker usually receives a percentage of the premium from the insurer. Generally, a broker will continue to earn commission so long as the policyholder maintains their policy, so it’s in the broker’s best interest to help find a policy that is the right fit.

Benefits of an Insurance Broker

What are the benefits of using an insurance broker to buy life insurance? Here are some key benefits of an insurance broker:

- A personalized experience. Finding the right life insurance policy can be challenging. A broker can offer a personalized experience, helping the client through the process and recommending policies that fit their individual needs.

- Quick rate comparisons. Comparing rates from different insurers is one key to finding the best price. A broker can do quick rate comparisons to help their clients find the best deals.

- Guidance. An insurance broker can use experience and knowledge to help provide guidance in selecting the best policy suited for the particular customer.

- Easier application process. Applying for life insurance can be time consuming and complex. A broker can help make the process easier.

Is a Life Insurance Broker Required to Buy Life Insurance?

No, you are not required to use a broker to buy a life insurance policy. A customer can buy a life insurance policy directly through an insurer or may use the services of an insurance agent. An insurance broker with life insurance experience, however, can be a great option to help to find the best policy for their clients’ specific needs.

The Bottom Line

Overall, a life insurance broker is a great way to find a life insurance policy that meets your needs. If you are looking to buy life insurance to help protect your family and loved ones, contact us at Acrisure to find a life insurance solution today or request a life insurance quote online now.

Determining which type of commercial insurance is right for a business can be overwhelming. While there are many types of policies to choose from, business hazard insurance can help ensure your business's longevity. Here you can learn more about business hazard insurance.

Determining which type of commercial insurance is right for a business can be overwhelming. While there are many types of policies to choose from, business hazard insurance can help ensure your business's longevity. Here you can learn more about business hazard insurance.

What Is Business Hazard Insurance?

Business hazard insurance, also known as “business property insurance” or “commercial property insurance,” helps protect small business owners in the event of damage to business property, typically buildings (owned or rented) as well as business equipment, caused by certain events. It can provide business owners with financial protection by covering property damage and also helps cover business interruptions caused by specific hazards.

Small business owners who own or rent space may be required by lenders or landlords to maintain small business hazard insurance to cover the physical property.

What Does Business Hazard Insurance Generally Cover?

Business owners should be aware of what business hazard insurance typically covers so they can make informed decisions about which policy will best suit their needs. While the terms, conditions and exclusions of each policy may vary, business hazard insurance policies typically cover losses to business property arising from the following events:

- Fire, smoke, and water damage

- Theft and vandalism

- Hail and lightning strikes

- Explosions or collapse

- Automobile or aircraft damage

If certain coverages are more important than others for a business, those can be discussed with a licensed insurance agent to help find cost-effective policy options based on any specific needs. It is important to make sure the business is adequately covered.

Is Business Hazard Insurance Necessary?

Although business hazard insurance may not be required in all states, it can be an important risk mitigation tool and should be considered when exploring business insurance needs. While helping business owners protect against losses to business property, business hazard insurance also provides business interruption coverage which helps protect a business against financial losses if it is forced to shut down due to a covered event. While the terms, conditions and exclusions of each policy may vary, business interruption coverage typically includes coverage for lost income or profits, costs to restore operations, operating expenses, loan payments and taxes.

Business Hazard Insurance vs. Homeowners Insurance

Another consideration when selecting the appropriate type of business property insurance is whether a business operates from a home office or commercial business site. If a business is operates out of a home, any homeowners insurance policy should be reviewed to determine whether business property may be covered and, if such coverage exists, whether it is sufficient or appropriate for the specific business needs. It is important to discuss coverage with the homeowners’ insurer as some carriers may require a separate business hazard policy be obtained for businesses that operate out of the home.

What Is the Difference Between Business Hazard Insurance and Commercial General Liability Insurance?

Business hazard insurance is a type of first party coverage that typically covers damage to the business owner’s commercial property resulting from specific risks or hazards, such as fire, theft, or natural disasters. Commercial general liability insurance, on the other hand, is a third-party liability policy which covers bodily injury, property damage and advertising injury caused to third parties, not the policyholder itself.

How Much Does Business Hazard Insurance Cost?

Many different factors may be considered by an insurance company when determining the premium cost for business hazard insurance. One main factor is the value of the property itself, including the physical building, the site where it sits and any physical business assets/equipment. Another important factor is whether the policy provides for replacement cost value (also called RCV) coverage or actual cash value (also called ACV) coverage.

Replacement cost value coverage in business hazard insurance refers to the cost needed to repair or replace damaged or destroyed property with new property of the same kind and quality without any reduction for depreciation. Actual cash value coverage, on the other hand, takes into account the property's depreciation and provides coverage for the cost to repair or replace the damaged property minus depreciation for age, condition and value. Business hazard insurance policies with actual cash value coverage are generally less expensive than those providing for replacement cost value coverage.

Do You Need Help Finding Hazard Insurance for Your Business?

Are you ready to find the right business hazard insurance policy for your business? Acrisure's licensed insurance agents specializing in business hazard insurance can help. Contact us for help finding a policy to suit your business needs or explore our other offerings and request a small business insurance quote online today.

Good News & Challenges

The Insurance Market Cycle: Hard Versus Soft Markets

The commercial insurance market is cyclical in nature, fluctuating between hard and soft markets. These cycles affect the availability, terms, and price of commercial insurance, so it’s helpful to know what to expect in both a hard and soft insurance market.

A soft market, which is sometimes called a buyer’s market, is characterized by stable or even lowering premiums, broader terms of coverage, increased capacity, higher available limits of liability, easier access to excess layers of coverage, and competition among insurance carriers for new business.

A hard market, sometimes called a seller’s market, is characterized by increased premium costs for insureds, stricter underwriting criteria, less capacity, restricted terms of coverage, and less competition among insurance carriers for new business.

Recent History – A 2023 Retrospective

Throughout 2023, the commercial insurance space became an increasingly complex environment. There’s been both good news and challenges.

In some lines of coverage—namely, directors and officers’ liability (D&O), employment practices liability (EPL), and workers’ compensation—shifting market dynamics, new capacity, and optimal underwriting results set the stage for improved conditions, which means fewer rate increases and, in some cases, rate decreases.

On the other hand, headwinds facing other coverage segments, such as commercial property and automobile led to diminished profitability and fueled double-digit rate hikes.

Looking ahead, industry experts anticipate that the commercial insurance sector will still carry challenges in 2024; however, it may present more favorable conditions than it has in previous years for some insurance buyers and in certain lines of coverage. Yet, some coverage segments, including commercial property and automobile will likely remain difficult to navigate. Regardless, a proactive approach to risk management in securing adequate coverage will be critical in securing needed insurance during this time. The key will be to address the factors we can control in advance.

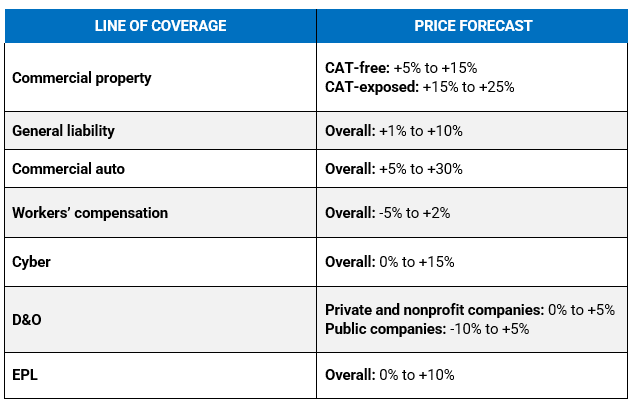

2024 Insurance Rate Forecast Trends

Price forecasts are based on industry reports and surveys for individual lines of insurance. Forecasts are subject to change and are not a guarantee of premium rates. Insurance premiums are determined by a multitude of factors and differ between businesses. Claims history will impact pricing and coverage availability. These forecasts should be viewed as general information, not insurance or legal advice.

Note: CAT refers to “catastrophic perils” such as wildfires, earthquakes, etc.

Your team here at Acrisure is ready to help. While the above predictions are based on expert research, they are subject to change. We encourage you to partner with us to learn price forecasts for your specific business and to set an insurance and risk management strategy that will maximize your protection and minimize cost. Let's have a conversation. Just reply here.

Generative artificial intelligence (AI) is garnering attention. Tools like ChatGPT draw from a wide database of information and language to create human-like text in response to various prompts.

Generative artificial intelligence (AI) is garnering attention. Tools like ChatGPT draw from a wide database of information and language to create human-like text in response to various prompts.

Since launching in November 2022, ChatGPT has acquired over 100 million active users. Given the popularity of ChatGPT and similar tools, companies across the globe are wondering how (or whether) to use them.

AI has helped companies create marketing content such as blog posts and social media updates, draft employee policies, and write simple contracts. ChatGPT can even integrate with existing customer service platforms to provide responses in interactive chats.

Many AI tools work by learning a user’s preferences and can receive training based on a company’s needs. This creates tremendous potential for using generative AI to your organization’s benefit. But you must know how to use it safely and properly. Before your company dives into a new AI use case, here are some key issues to be aware of:

The legal implications of using generative AI tools are still forming

Harvard Law School recently released an article titled “The Implications of ChatGPT for Legal Services and Society.” The article argues that one of the challenges to using generative AI tools is their inability “to account for the nuances and complexities of the law.” This may not seem like a big deal to a user looking for a basic answer to a basic question. However, businesses should be careful when taking advice from AI tools or using AI to create contracts, provisions, policies, or other documents with legal force.

For example, suppose a human resources manager asks AI to generate a sick leave policy for employees with mental health issues. The AI tool may produce something that appears coherent and structurally correct, but it’s unlikely to be legally compliant. AI tools frequently fail to consider all relevant factors, including the many details and facets of federal, state, and local laws.

The intersection between AI tools and intellectual property law is still murky

ChatGPT and similar AI platforms aggregate information from available internet sources. While AI content is technically original, it may violate another party’s copyright or otherwise run afoul of intellectual property laws. This problem is compounded by the fact that AI often can’t reliably cite its sources.

A related issue is that U.S. copyright laws have not yet caught up with AI technology. According to ChatGPT’s creator, OpenAI, users retain the legal rights to any inputs they provide, but the ownership of outputs is not yet clear.

Before allowing companywide use of generative AI tools, consider privacy

AI can help you reduce response times, handle basic customer service requests, and even manage schedules, but it’s only as helpful as the information you put in.

And you must be extremely cautious about the information you put in. Although ChatGPT’s privacy policy promises to only share input data to provide its services and never sell input data, it still cautions users not to put sensitive data into its chat box.

Data put into ChatGPT is saved for a period of time, which may expose it to hackers looking to exploit your information. You can protect your company’s and clients’ sensitive information by enforcing a companywide policy of never putting sensitive data into AI tools.

You may wish to take a risk-averse position and refrain from using client names. But if you do choose to use client names (for market, industry, or competitor research), you might consider amending your privacy policy to include the use of certain client data for AI-assisted research purposes.

Generative AI tools like ChatGPT don’t always produce accurate answers

As previously discussed, generative AI tools like GhatGPT can’t reliably cite the sources used to collect data or produce responses. Further, many popular AI platforms work off a stagnant set of data, meaning you won’t get the most up-to-date information in response to your prompt.

Perhaps most troubling, generative AI tools have been known to produce responses that are biased, incendiary, or just plain incorrect. You should always carefully fact-check outputs before using them internally or externally.

SEO is catching up to AI-generated content

Search engines may not penalize you for using AI-generated content now, but they might in the future. You must continue to weigh the pros and cons of using AI-generated content with the expectation that search engines like Google may change their policies.

In April 2023, RockContent reported that “Google is not giving you blanket permission to generate poor-quality content with these tools just for the purpose of tricking the search engines into ranking you higher.”

Furthermore, Business Insider reports that Google is planning to debut a new feature allowing users to identify if an image is real or AI-generated.

VANTREO- Acrisure is here to help. The AI landscape is shifting rapidly, with new use cases uncovered every day. Many small and midsize businesses are seeking outside help with making AI tools work for them. If you have questions regarding AI risk or how insurance does and does not apply to AI business use, please reach out to your legal counsel or ask just Reply here.

Over the past 25 years, more than 940 children have died of heatstroke (30 to 55 children die each year) as a result of being left or trapped inside a car.

Here are some other notable trends from the National Highway Traffic Safety Administration:

Here are some other notable trends from the National Highway Traffic Safety Administration:

• About 46% of the time, the caregiver intended to drop off the child at a daycare or preschool but inadvertently forgot them in the car.

• Thursdays and Fridays, signaling the end of the workweek, have witnessed the highest number of heatstroke-related deaths.

• In 53% of hot car deaths, someone forgot a child inside a vehicle.

• More than half (54%) of hot car deaths involve children under the age of 2.

These statistics emphasize the urgent need to raise awareness about the dangers of vehicle-related heatstroke and the precautions that must be taken to prevent such tragedies.

Important Precautions – Everyone Can Help Prevent Hot Car Deaths

1. Never leave a child in a vehicle unattended for any length of time. Rolling the windows down or parking in the shade does little to change the interior temperature of the vehicle.

2. Make it a habit to check your entire vehicle — especially the back seat — before locking the doors and walking away.

3. Ask your childcare provider to call if your child doesn’t show up for care as expected.

4. Place a personal item like a purse or briefcase in the back seat as another reminder to look before you lock. Write a note or place a stuffed animal in the passenger's seat to remind you that a child is in the back seat.

5. Store car keys out of a child's reach and teach children that a vehicle is not a play area